- Opening Bell Daily

- Posts

- Inflation isn't cooling but the Fed will likely cut rates anyway

Inflation isn't cooling but the Fed will likely cut rates anyway

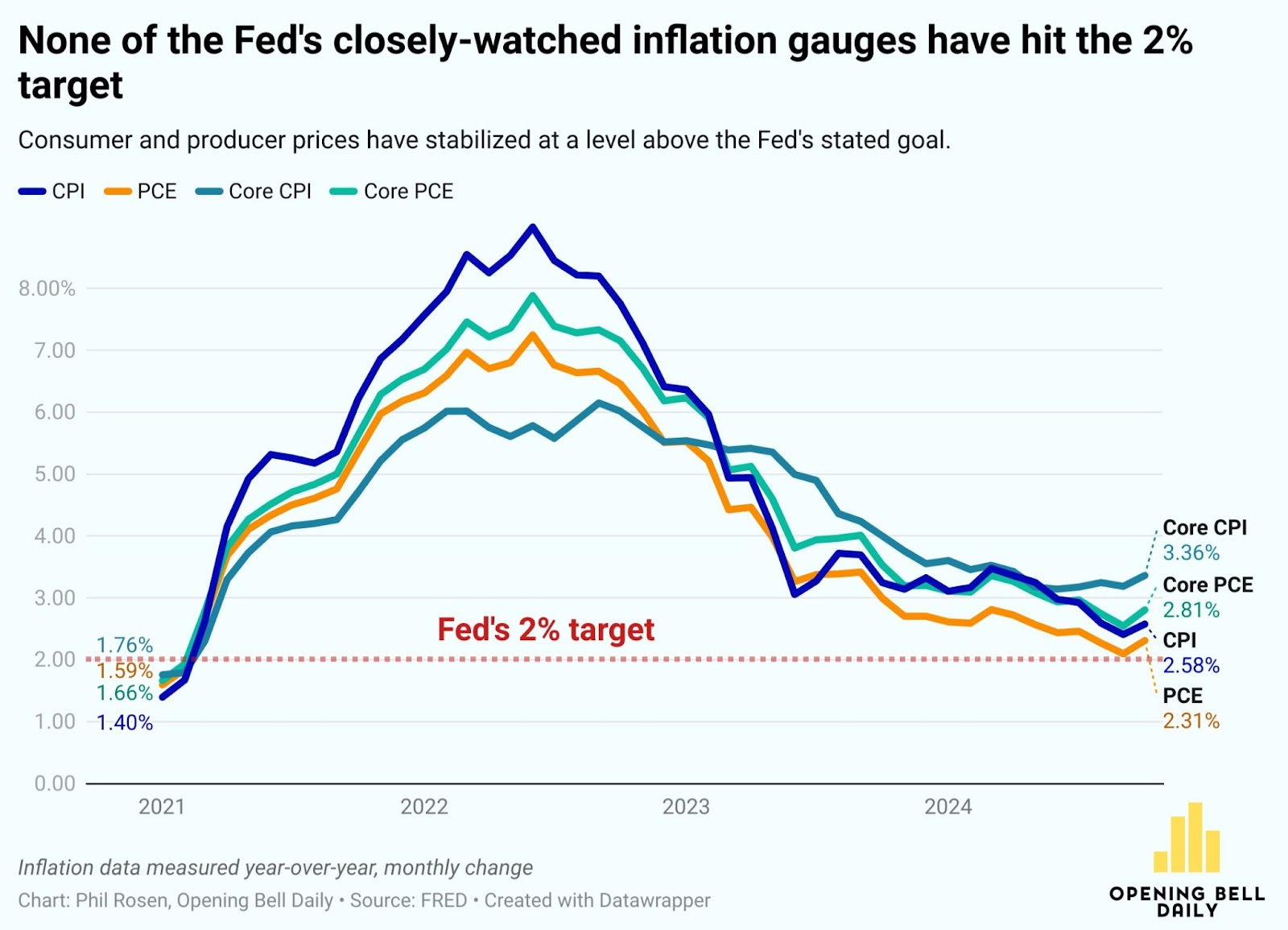

None of the key economic data has fallen into the central bank's target range.

Phil Rosen

December 11, 2024

Good morning! It’s not entirely clear right now who is steering economic policy: The Federal Reserve or financial markets.

Let’s break it down.

Today’s letter is brought to you by Public!

You’ve probably heard a lot about interest rates in the news lately. But even as rates start to fall, there’s still time to earn some of the highest yields we’ve seen in years.

Public.com is a powerful platform for investors who are serious about putting their money to work.

A quick rundown of what you can get with Public:

The High-Yield Cash Account: 4.35%* APY with zero fees and up to $5M FDIC insurance

The Treasury Account: Lock in a guaranteed yield with US Treasuries — widely considered one of the safest investments for your portfolio

The Bond Account: Secure a yield of 6%** or higher.

If you’re looking to earn steady interest — even as rates change — head to Public.

The Fed wants to avoid surprises

Economists and market commentators across the board expect the Federal Reserve to lower interest rates by 25 basis points on December 18, yet it’s difficult to decipher whether recent economic data justify the move.

Putting aside the forecasts for November inflation, the last handful of reports have underscored just how hard it is to cool a hot economy.

“The Fed has cut the federal funds rate more than enough,” strategists from Yardeni Research said Tuesday.

Indeed, consumer prices and personal consumption expenditures remain above the Fed’s stated target of 2%.

The final CPI report of the year is also seen moving higher, not lower.

Meanwhile, the November employment report suggests the labor market remains relatively robust.

“With both sides of the Fed’s dual mandate (stable prices and full employment) heating up, it’s increasingly likely that the Fed has cut the federal funds rate by too much, too soon,” said Yardeni’s chief markets strategist Eric Wallerstein.

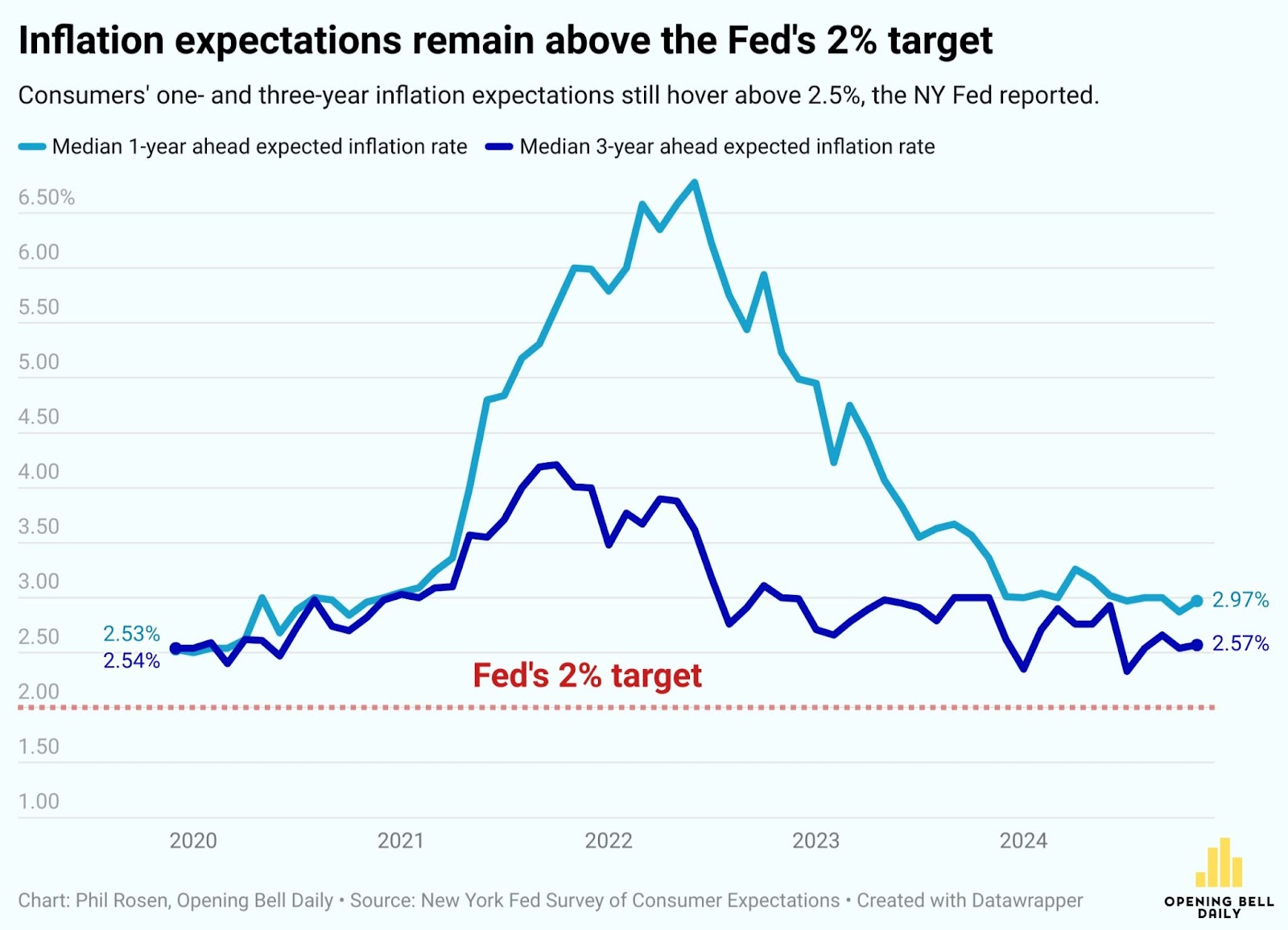

Notably, a Monday survey from the Federal Reserve Bank of New York showed that consumers don’t expect inflation to fall to 2% for at least the next three years.

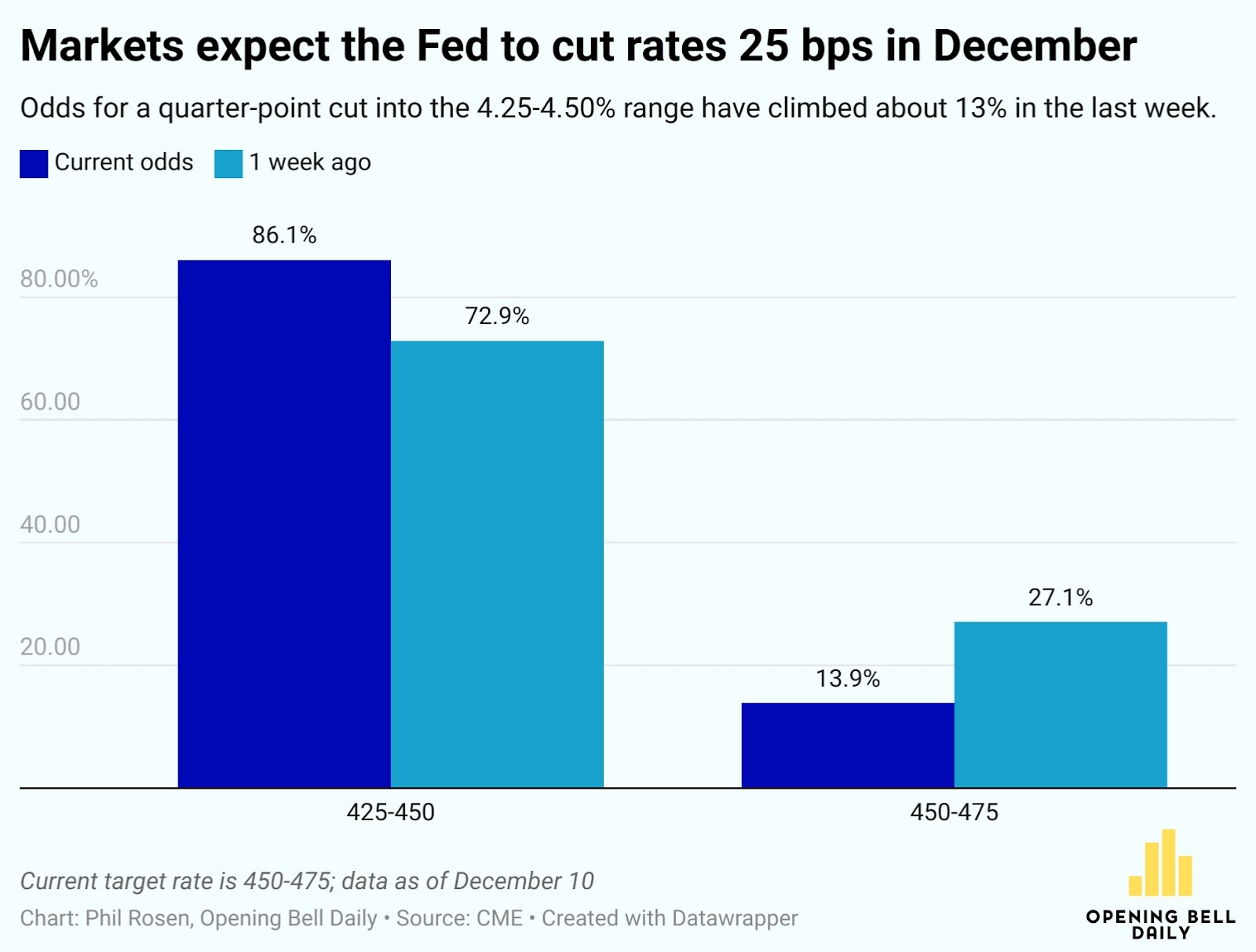

All the while, traders have steadily ramped up their bets for a December rate cut, with odds for a quarter-point cut jumping from 72% to 86% over the last week, according to CME data.

Two questions come to mind as the Fed prepares to lower rates into the 4.25-4.5% range:

Will policymakers cut rates because of the economic data?

Will policymakers cut rates because they don’t want to run counter to overwhelming market expectations?

Broadly speaking, the central bank lowers interest rates to stimulate the economy during periods of sluggish spending and weak economic activity.

Conversely, when consumer spending ramps up and inflation accelerates, the Fed raises rates to curb excessive price growth.

In this instance, however, the Fed’s next move could very well be driven by its aversion to surprising markets.

Comments or feedback? Reply directly to this email or let me know on X @philrosenn.

Elsewhere:

📉Stocks dropped for a second day. All three major US indexes finished Tuesday lower as investors braced for the November CPI report, due Wednesday morning. Still, some investors are still preparing for the seasonal Santa Rally to hit in the coming weeks.

♨️ Inflation is expected to come in hot. The November CPI report, due this morning, is seen coming in at 2.7% year-over-year, hotter than the 2.6% seen the prior month. Core CPI, which strips food and energy, is expected to hold at 3.3%. If those estimates hold, it would mark the third month in a row of rising inflation, and the highest headline print since July (Opening Bell Daily)

❌ Microsoft doesn’t want bitcoin. MicroStrategy founder Michael Saylor, arguably the most prominent bitcoin evangelist, has been encouraging the tech giant to follow his lead and buy the crypto. Shareholders on Tuesday rejected that idea, as a formal proposal failed to garner support. (CNBC)

Rapid-fire:

Alphabet stock surged after Google unveiled “Willow,” a quantum computing chip (CNBC)

Walgreens is in talks to sell itself to a private-equity firm (WSJ)

Wall Street’s relentless appetite for returns has triggered the biggest boom for complex financial products since 2007 (FT)

Zillow forecasts that even a wave of boomer home sales won’t fix the housing affordability crisis (Business Insider)

A court blocked Kroger’s $25 billion acquisition of grocery rival Albertsons (CNBC)

The arrest warrant for the UnitedHealth CEO’s alleged killer details how law enforcement tracked down the suspect (WSJ)

MicroStrategy now owns 2% of all bitcoin that will ever be in circulation (Pomp Letter)

Last thing:

The share of Americans who expect they will be better off financially over the coming year jumped in November to its highest level since the Covid-19 pandemic, according to the NY Fed's consumer survey

— Nick Timiraos (@NickTimiraos)

4:00 PM • Dec 9, 2024

Interested in advertising in Opening Bell Daily? Email [email protected]

Disclosures:

** As of [9/16/24], the average, annualized yield to worst (YTW) across all ten bonds is greater than 6%. A bond’s YTW is not “locked in” until the bond is purchased and is not guaranteed; you may receive less than the YTW of the bonds in the Bond Account if you sell any of the bonds before maturity or if the issuer defaults on the bond.

Paid endorsement for Public Investing, Inc. Not investment advice. All investing involves the risk of loss, including loss of principal. Brokerage services for US-listed, registered securities, options and bonds in a self-directed account are offered by Public Investing, Inc., member FINRA & SIPC. Public Investing offers a High-Yield Cash Account where funds from this account are automatically deposited into partner banks where they earn interest and are eligible for FDIC insurance; Public Investing is not a bank.

Treasury accounts offering 6 months T-Bills are offered by Jiko Securities, Inc.,member FINRA & SIPC. Securities in your account are protected up to $500,000. For details: www.sipc.org. Banking services and the Bank Accounts are provided by Jiko Bank, a division of Mid- Central National Bank. For U.S. Investments in T-bills: Not FDIC Insured; No Bank Guarantee; May Lose Value. Treasuries risk disclosures, see https://jiko.io/docs/treasuries_risk_disclosure.pdf. See public.com/#disclosures-main

A Bond Account is a self-directed brokerage account with Public Investing, member FINRA/SIPC and includes 10 investment-grade and high-yield bonds. As of [11/08/24], the average, annualized yield to worst (YTW) across all ten bonds is greater than 6%. A bond’s YTW is not “locked in” until the bond is purchased and is not guaranteed; you may receive less than the YTW of the bonds in the Bond Account if you sell any of the bonds before maturity or if the issuer defaults on the bond. While corporate bond yields should fall in reaction to a Federal Reserve rate cut, there is no way to know whether that will be true of the bonds in the Bond Account, how quickly bond yields will respond, or by how much they will decline. Bond Accounts are not recommendations of individual bonds or default allocations. The bonds in the Bond Account have not been selected based on your needs or risk profile. All investing involves risk. Public Investing charges a markup on each bond trade. Visit public.com/bond-account to learn more

Reply